Early Retirement FIRE Number Calculator

Based on the Trinity Study 4% Safe Withdrawal Rule. Calculate how much you need to invest monthly to retire early, adjusted for inflation and compounding interest.

Timeline & Lifestyle

Growth & Withdrawal Rates

🎉 Congratulations!

You've already reached your target FIRE Number. You can technically retire today!

Target FIRE Number

- -

Achieve by Year --

Monthly Investment

- -

Required to hit your goal.

Retirement Need

* Adjusted for your selected inflation rates.

Investment Trajectory

The Early Retirement FIRE Number Calculator is a financial planning tool that calculates the exact portfolio value you need to retire early and the monthly investment required to reach it. It applies the Trinity Study 4 percent Safe Withdrawal Rate, adjusts for general and healthcare inflation, projects compound growth, and converts results into 12+ global currencies for accurate FIRE planning.

Why a FIRE Number Is the Single Most Important Figure in Early Retirement Planning

Your FIRE number is the portfolio threshold at which passive investment returns can sustain your lifestyle indefinitely without requiring active income. The concept emerged from the Trinity Study, a 1998 academic paper by three Trinity University professors that analyzed historical market data and concluded that retirees withdrawing 4 percent of an inflation-adjusted portfolio annually had a high probability of preserving capital across a 30-year horizon.

Financial Independence, Retire Early (FIRE) communities have refined this concept into actionable subcategories: Lean FIRE (under $1 million portfolio for minimalist living), Fat FIRE (over $2.5 million for upscale retirement), Coast FIRE (a partially funded portfolio that grows to full FIRE through compounding alone), and Barista FIRE (semi-retirement supplemented by part-time income). Each variant uses the same core math but adjusts the input variables.

The U.S. Internal Revenue Service treats most FIRE-funding accounts (401(k), Roth IRA, taxable brokerage) under distinct withdrawal and contribution rules, and consulting IRS Publication 590-B is recommended for tax-aware retirement planning. Knowing your FIRE number transforms abstract retirement anxiety into a concrete, measurable savings goal.

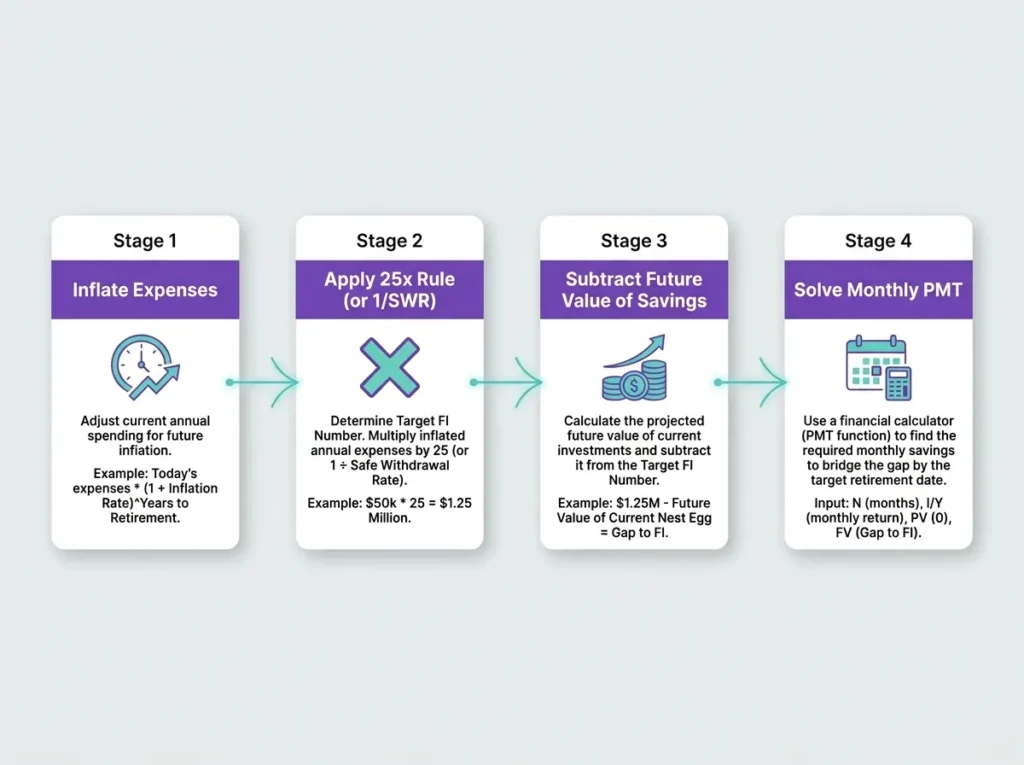

The Logic Behind the FIRE Number Calculation

The Standard FIRE engine uses the Trinity Study 4 percent rule, which is mathematically equivalent to multiplying annual expenses by 25. The Advanced engine separates pre-retirement return, post-retirement return, healthcare inflation, and a custom Safe Withdrawal Rate (SWR).

Core FIRE Number Formula (Standard Mode):

FIRE Number = (Inflated Annual Expenses) / SWR

= (Current Monthly Expenses x 12 x (1 + i)^n) / 0.04Required Monthly Investment (PMT) Formula:

PMT = (FV - PV x (1 + r/12)^(n x 12)) x (r/12) / ((1 + r/12)^(n x 12) - 1)Where:

- FV = Target FIRE Number (future value)

- PV = Current Saved/Invested Balance

- r = Pre-Retirement Annual Return (decimal)

- n = Years until retirement (Target Age minus Current Age)

- i = General Inflation Rate (decimal)

Advanced Mode Healthcare Adjustment:

Inflated Monthly Need = (Non-Healthcare Expenses x (1 + i_general)^n)

+ (Healthcare Expenses x (1 + i_healthcare)^n)When This Calculation Doesn’t Apply: The 4 percent rule was modeled on U.S. equity and bond data over a 30-year horizon. If your retirement period exceeds 40 years, your portfolio holds significant non-correlated assets (real estate, private equity, crypto), or you face hyperinflationary jurisdictions, the Standard mode may produce optimistic results. Use Advanced mode with a 3 to 3.5 percent SWR for conservative perpetual-withdrawal scenarios.

FIRE Number Reference Table by Annual Spending

Standard FIRE targets calculated using the 25x rule (4 percent SWR), excluding inflation adjustments.

| Annual Expenses (USD) | FIRE Number (25x) | Lean / Fat Classification | Monthly Withdrawal at 4% SWR |

|---|---|---|---|

| $25,000 | $625,000 | Lean FIRE | $2,083 |

| $40,000 | $1,000,000 | Standard FIRE | $3,333 |

| $60,000 | $1,500,000 | Standard FIRE | $5,000 |

| $80,000 | $2,000,000 | Standard FIRE | $6,667 |

| $100,000 | $2,500,000 | Fat FIRE Threshold | $8,333 |

| $150,000 | $3,750,000 | Fat FIRE | $12,500 |

| $200,000 | $5,000,000 | Chubby/Fat FIRE | $16,667 |

Practical Scenario: Salma’s 20-Year FIRE Plan in JPY

Salma is a 30-year-old software engineer based in Tokyo who currently spends $5,000 USD/month, with $500 of that allocated to healthcare. She has $50,000 already invested and wants to retire by age 50. She uses Advanced mode with 8 percent pre-retirement return, 3 percent general inflation, 5 percent healthcare inflation, and a 4 percent SWR.

Step 1: Inflate monthly expenses across 20 years

- Non-healthcare: $4,500 x (1.03)^20 = $8,127

- Healthcare: $500 x (1.05)^20 = $1,327

- Total inflated monthly need: $9,454 (which the tool displays as ¥1,490,600 at the live rate)

Step 2: Annualize and apply SWR

- Annual need: $9,454 x 12 = $113,448

- FIRE Number: $113,448 / 0.04 = $2,836,200

Step 3: Convert to display currency

- $2,836,200 x 157.6662 JPY/USD = ¥447,179,943

Step 4: Solve for monthly PMT

- Future value of $50,000 at 8% over 20 years = $233,048

- Gap to fund: $2,836,200 – $233,048 = $2,603,152

- Monthly PMT (8%, 240 months): approximately $4,397, which equals ¥693,253

Salma’s tool output confirms a target of ¥447,179,943 with a required monthly investment of ¥693,253 to retire on schedule.

How to Use the Early Retirement FIRE Number Calculator (Step by Step)

- Choose your engine. At the top of the calculator, click either “Standard FIRE (4% Rule)” for a quick Trinity Study projection or “Advanced FIRE (Custom Rates)” to adjust returns and healthcare inflation independently.

- Fill in Timeline & Lifestyle. Enter your Current Age, Target Retirement Age, Current Monthly Expenses (in your base currency), and Current Saved/Invested Balance. In Advanced mode, also enter the healthcare portion of your monthly spending and a healthcare inflation rate.

- Set Growth & Withdrawal Rates. Standard mode locks the SWR at 4 percent. Advanced mode lets you input separate pre-retirement and post-retirement return rates plus a custom SWR (3 to 5 percent is the common range).

- Pick currencies. Select your Base Calculation Currency (the currency your inputs are denominated in) and your Convert Entire Plan To currency. The dropdown supports USD, EUR, GBP, JPY, INR, AED, and 8+ others, with live FX rates fetched at calculation time.

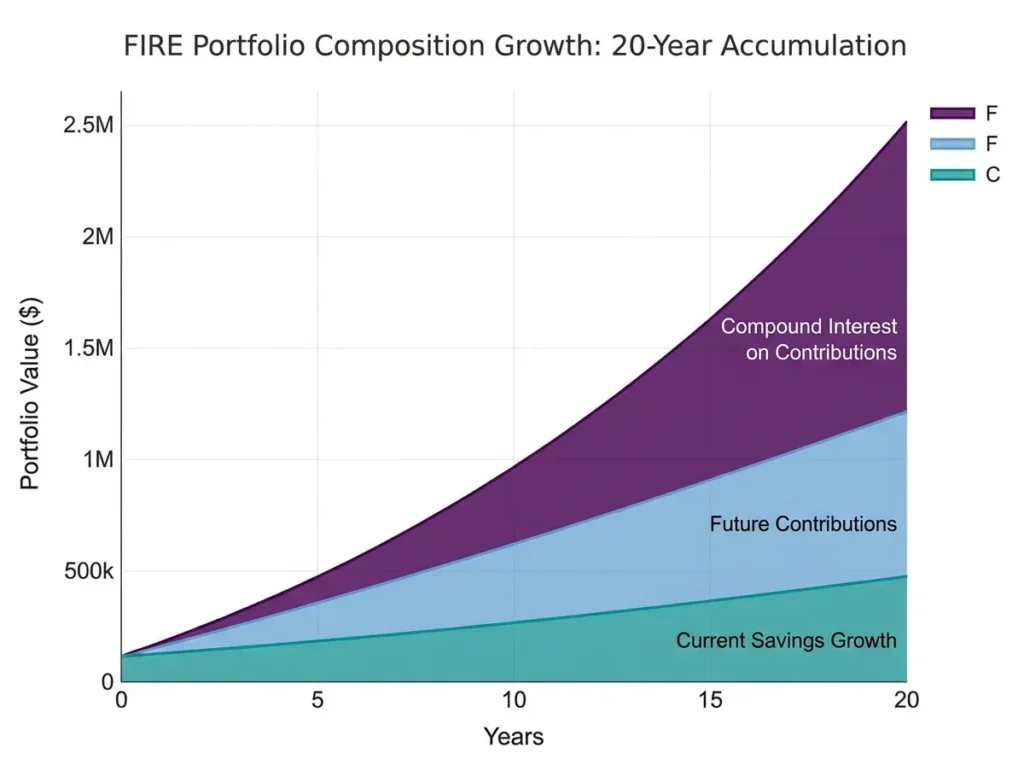

- Click Calculate FIRE Number. Review the Target FIRE Number, Monthly Investment requirement, donut chart of portfolio composition, and the Investment Trajectory breakdown showing how much of your nest egg comes from current savings, future contributions, and compound interest.

- Iterate or share. Use Reload Calculator to start over, Copy URL to Share to save your scenario as a permalink, Print Report for a clean PDF, or Email Result to send the snapshot to yourself. Two cross-link buttons let you jump to the 401k vs Roth IRA Comparison or the Social Security Break-Even Calculator for deeper planning.

For users who want to compare tax-advantaged account growth before locking in their FIRE strategy, the 401(k) vs Roth IRA Future Value Comparison Calculator models pre-tax versus after-tax compounding, while the Social Security Break-Even Age Calculator helps optimize the claiming age that complements your FIRE drawdown.

Frequently Asked Questions

What is a realistic FIRE number for a middle-income U.S. household?

For a household spending $60,000 annually, the standard FIRE number is $1.5 million using the 25x rule. Adjusting for 3 percent inflation over a 20-year accumulation phase pushes the inflation-adjusted target closer to $2.7 million in nominal future dollars, which the calculator computes automatically.

Is the 4 percent Safe Withdrawal Rate still safe in 2026?

The 4 percent rate remains the most cited benchmark, though recent retirement researchers including Wade Pfau and Michael Kitces suggest 3.3 to 3.5 percent for retirements exceeding 40 years or starting during high equity valuations. The Advanced mode lets you stress-test your plan at lower SWRs.

How does healthcare inflation impact my FIRE number?

Healthcare costs in the U.S. have historically inflated at roughly 5 to 6 percent annually, nearly double general CPI. For a household spending $1,000/month on healthcare today, inflating that line at 5 percent over 25 years produces a future need of about $3,386/month, materially increasing the required portfolio.

Calculate your personalized FIRE number now and turn your early retirement dream into a dated, dollar-precise roadmap.

Formula accuracy verified for standards.